Leasing Vs. Financing – Know The Facts

You already know that you’re ready to buy a vehicle. You’re deciding what you need your vehicle for, how much space you’ll need, whether you prefer a manual or automatic transmission and if you’ll actually be able to parallel park anything larger than a sedan. When you select some possible options, you’ll probably take a look at prices and decide whether you can afford a new vehicle or a used one. Here, fellow car shoppers, is where the situation can get a little tricky. The question will definitely arise during your car shopping experience: Should you lease or finance your next car?

This isn’t a decision that should be taken lightly since it has a huge impact on your finances for years to come. So how do you decide between leasing and financing? Well, you’re in luck – AutoLoans.ca can help you get informed so that you can make the best decision possible! Let’s get started!

LEASING

When leasing a vehicle, you’re essentially renting it for several years, because at the end of the lease, the car is returned to the dealer. There are both pros and cons to this practice, so make sure to consider them all before deciding to lease your next vehicle.

Pros

Yes, you’ll likely have lower monthly payments if you lease your car, but that’s because the loan amount is only for the amount the car will depreciate over the length of the lease. With a lease, you are only financing “the difference between the purchase price and the residual value.” Leasing also means that you’ll pay less tax since only your monthly payments are taxed, not the full vehicle cost (Car Choice Canada). You also shouldn’t have to worry much about repairs when you lease a car; most leasing contracts stipulate that the vehicle is required to be regularly serviced, usually by the manufacturer. You will have to foot the bill for this regular maintenance, but it’s worth trying to negotiate on this point with the dealer. A lease is also a better option if you’re all about driving the newest model, because it only lasts approximately three to four years and then you can pick up your next new vehicle.

Cons

A lease may seem like the perfect cheap option to get back on the road without scaring your wallet, but be warned, leases also come with some strings attached. When you lease a car, be sure to read that fine print, because otherwise, you could be left on the hook for some hefty charges. Do you like to drive and tend to take long road trips? Then a lease probably isn’t the best option for you. There is an annual mileage limit for a leased vehicle and if you exceed the mileage allowed, you will be charged per extra kilometre.

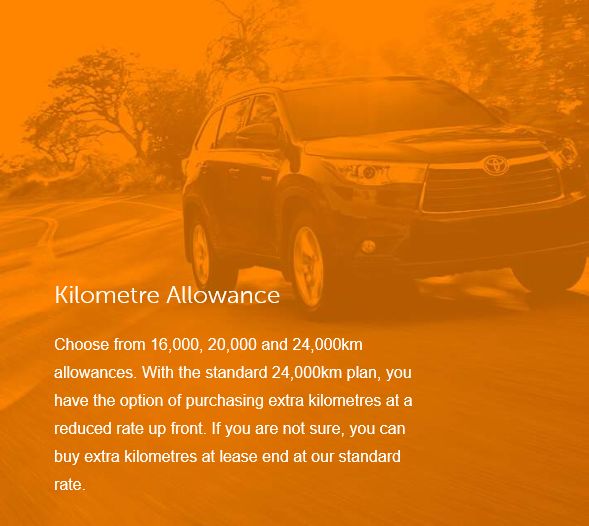

Check out Toyota Canada’s mileage restriction options for lessees (other car manufacturers may have different mileage limits):

There may also be travel restrictions hidden in the fine print; be clear on whether or not you will need the Lessor’s permission to take your new ride on a road trip out of the country. When you lease a vehicle, the manufacturers do expect to see some minor wear and tear after you return it. But if that damage exceeds what is expected, then “customers may face a steep bill.” Finally, when entering into a lease, please be certain that you’re comfortable with its length, because trying to terminate the contract early can “trigger a hefty penalty”.

FINANCING

Financing a vehicle (aka. getting a car loan) means that you will be buying it and after the loan is fully paid off, you will own it. By considering the benefits and drawbacks of financing, you can determine whether it’s the better option for your next car.

Pros

First off, when you buy a car, it’s totally yours! After you sign the papers and drive it off the lot, you can buy some spinning rims, tint your windows and put on a black matte wrap (if that’s your thing). You will still make monthly payments towards your car loan, but you can pay off your loan faster by making extra payments. Car loan terms can last from one to eight years, so you can choose a term that will allow your monthly payments to fit your budget. When you decide to buy instead of a lease, you’re able to choose a car that’s up to seven years old as long as it’s $7,500 (taxes included) or more. Since the car is yours to use as you please, there are no mileage or travel restrictions to consider. There are also no maintenance schedules to adhere to but according to The Globe and Mail, “for the most part, a person who drives responsibly and pays attention to routine maintenance is going to come out ahead if they buy.”

Cons

Financing a car is definitely a bigger commitment than leasing a vehicle; you could have your vehicle for the next 10 to 15 years! Also, when you buy a vehicle, you apply for financing for the entire value of the car, so your loan will likely be larger than someone who leases and therefore, your monthly payments will also be higher than a lessee’s. It makes sense then that you also pay more taxes since you’re taxed on the full amount of the car, not just the amount it depreciates while you drive it. Again, you’ll have to handle the maintenance costs, but you should be prepared to make repairs since you’ll probably have the car longer than a lease term. When buying your next car, make sure that you’re also prepared for more time at the mechanic’s if you decide to purchase an older model vehicle. Another downside of buying your next car is not being able to get a new car every few years with the newest automotive technology to help you along on your commute. But being upset over this minor point is the definition of #firstworldproblems.

If you’re still not sure whether you want to lease or finance your next vehicle, maybe checking out the costs associated with both options will sway your decision. This Government of Canada website has something helpful called a Vehicle Lease or Buy Calculator. You can use this tool to “compare the costs to finance, lease or lease/buyout a vehicle over time”.

In the event that you’ve made the decision to finance your next vehicle (I knew that black matte wrap sounded fun), get in touch with the friendly and knowledgeable staff at AutoLoans.ca or start your application for financing here.

In the event that you’ve made the decision to finance your next vehicle (I knew that black matte wrap sounded fun), get in touch with the friendly and knowledgeable staff at AutoLoans.ca or start your application for financing here.